Targeted Review Summary

In the latter half of 2019, the XRB conducted a Targeted Review of the New Zealand Accounting Standards Framework (ASF) and issued a Discussion Paper to

receive feedback.

This Targeted Review Summary accompanied the Discussion Paper, and outlined the key objectives of the review, identified three specific areas that needed feedback, as well as what was outside the scope of the targeted review.

For more information, you can view the full discussion paper, or the summary document.

We've also explained the issues and how this affects you in a webinar, which was held on 21 August 2019.

Why a targeted review of the New Zealand Accounting Standards Framework (ASF)?

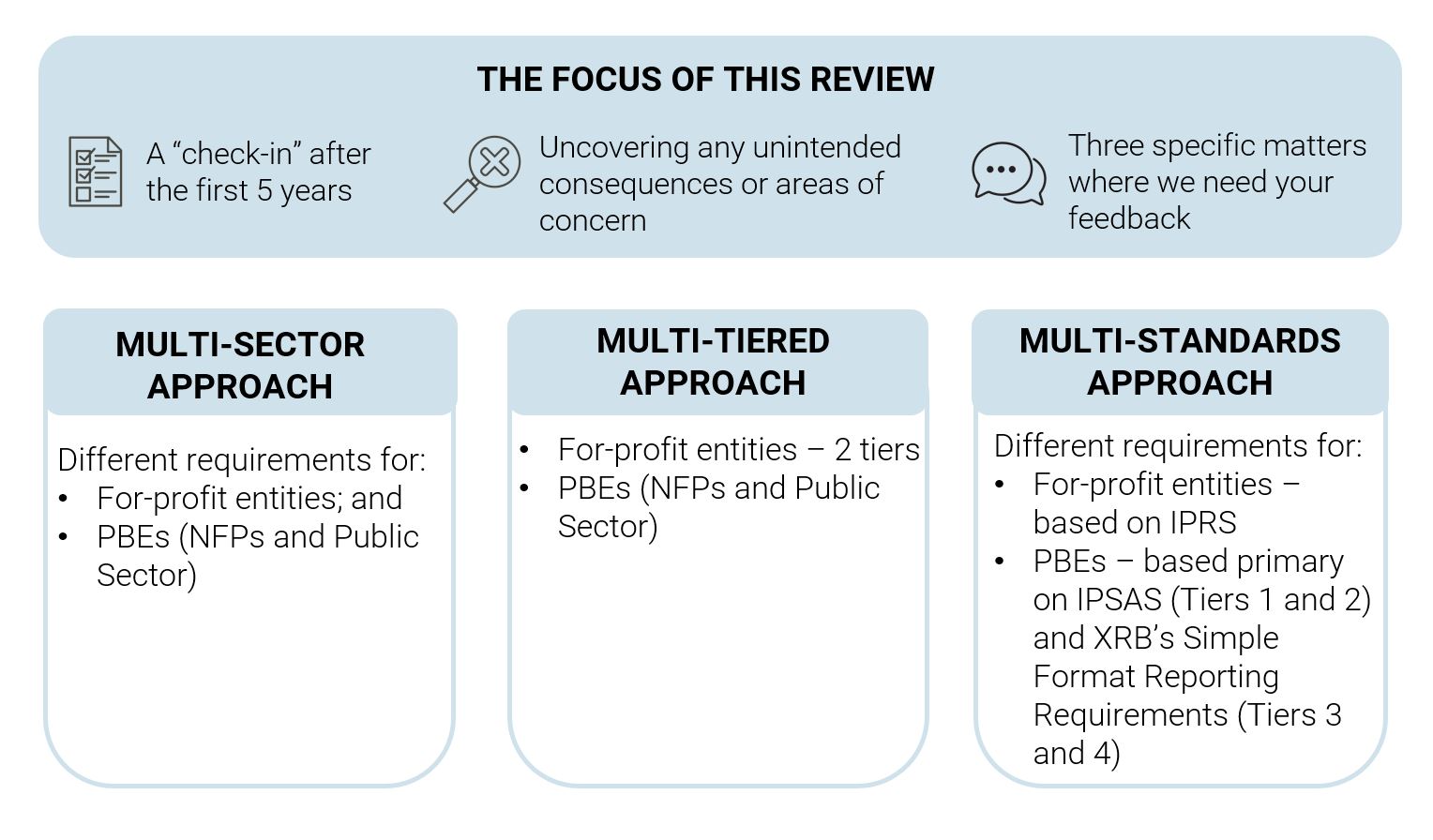

Now that the ASF has been effective for 4–5 years for many entities, the XRB considered it was timely and important to “check-in” with users of the framework and other stakeholders to receive feedback on whether the ASF had been functioning as anticipated and was achieving its original objectives.

More information: What is the accounting standards framework?

What were the objectives and scope of the consultation?

This was not a first-principles review.

The XRB considered it was too soon to conduct a first-principles’ review of the ASF as it was first issued only in 2012 and had introduced significant change for many entities. Also, we were not aware of significant unintended consequences arising from the implementation of the fundamental elements of the ASF.

Therefore, this review did not contemplate changing the ASF’s multi-standards, multi‑tiered approach, or which international standards are used as a base for developing standards in New Zealand.

The XRB expects to review these fundamental elements once the ASF has been effective for at least 10–15 years.

Key objectives of the targeted review of the New Zealand Accounting Standards Framework

The key objectives were to check-in on whether:

- the ASF was functioning as anticipated and had been achieving its desired objectives;

- there were any unintended consequences or concerns to date arising from the implementation of the ASF; and

- any refinements to the ASF were needed because of any new developments or emerging issues since the ASF was first developed.

Specific Matters for Comment (SMCs)

As well as seeking general feedback on whether the current ASF was functioning as anticipated, the XRB identified three specific matters for further feedback.

A summary of each specific matter for comment (SMC) is set out below.

PBE Standards for Tier 1 and Tier 2 NFP and public sector PBEs have been closely based on international standards – IPSAS – issued by the International Public Sector Accounting Standards Board (IPSASB).

While this strategy was effective in establishing the PBE Standards and the XRB planned to continue using IPSAS when developing future changes to PBE Standards, there had been some challenges in implementing the current strategy of maintaining close alignment between PBE Standards and IPSAS moving forward.

The XRB’s strategy focuses on maintaining close alignment between PBE Standards and IPSAS and, therefore, it aimed to avoid making changes to PBE Standards ahead of the IPSASB issuing final standards on the same topic. However, the time taken by the IPSASB to complete its projects to develop IPSAS based on recently‑issued IFRS Standards had been longer than expected.

This has led to an extended period of unnecessary divergence between PBE Standards and the standards applied by for-profit entities in New Zealand (i.e. NZ IFRS). This delay is particularly problematic for “mixed groups”, which include both for-profit entities and PBEs in the same consolidated group.

Also, while the current strategy has provided some flexibility to modify IPSAS requirements for New Zealand-specific considerations, there has been a relatively high hurdle to jump before making such modifications. This has made it challenging to adequately reflect local considerations to ensure that PBE Standards are “fit for purpose” in New Zealand.

The IPSASB’s workplan now includes large public sector-specific projects. While work on these important topics is welcomed, the IPSASB is required to consider the needs of a wide range of constituents – including countries transitioning from cash accounting. Many of the IPSASB’s constituents are very different to New Zealand constituents.

Therefore, the needs of New Zealand constituents might not be fully or appropriately addressed by future IPSAS that address public sector‑specific issues in the international environment.

The XRB is therefore considering whether its current strategy of maintaining close alignment between PBE Standards and IPSAS should be relaxed, to provide more flexibility in how IPSAS is used in the future when developing new or amended PBE Standards, including more flexibility on:

- the timing of when new or amended PBE Standards are introduced (e.g. not necessarily waiting for the IPSASB); and

- whether to adopt or modify the requirements of a new or amended IPSAS to reflect local considerations.

A more flexible approach is likely to result in less alignment between PBE Standards and “pure” IPSAS in the future, compared with the current strategy. Hence, the XRB was seeking feedback to help it consider whether it could move to a more flexible approach.

Further information can be found here.

[1] For example, the IPSASB is currently working on projects to develop standards based on IFRS 15 Revenue from Contracts with Customers and IFRS 16 Leases. Both IFRS 15 and IFRS 16 have recently become effective for for-profit entities.

For-profit entities that are required by law to prepare financial statements in accordance with standards issued by the XRB, but do not meet the criteria for Tier 1[2], are in Tier 2. Under the ASF, for-profit entities in Tier 2 apply NZ IFRS with Reduced Disclosure Requirements (RDR). The disclosure requirements for Tier 2 for‑profit entities have been harmonised with Australia. However, the Australian Accounting Standards Board (AASB) has considered a new approach to setting Tier 2 disclosure requirements.

Furthermore, the International Accounting Standards Board (IASB) recently began a project on small and medium entities that are subsidiaries of entities that report under IFRS Standards (“SMEs that are subsidiaries”). This project may result in a set of accounting requirements that could be suitable as a replacement for the current Tier 2 regimes in both New Zealand and Australia. However, the IASB is unlikely to complete this project before the new approach to Tier 2 disclosures is introduced in Australia.

If the developments in Australia were to result in some loss of trans-Tasman harmonisation for Tier 2 for-profit disclosures, the XRB would then need to consider introducing similar changes in New Zealand. Another matter was whether it is more cost-effective for New Zealand to delay changes until an international solution becomes available, to avoid two rounds of changes.

Further information can be found here.

[2] Tier 1 includes for-profit entities that are publicly accountable (defined next) and public sector for-profit entities with expenses over $30 million.

The PBE tier size criteria have not changed since the framework was first introduced. The XRB was therefore taking this opportunity to check-in with stakeholders on whether there were any unintended consequences or recent developments that would require the threshold to be revisited.

|

PBE Tier |

Tier Size Threshold |

|---|---|

|

1 |

Annual expenses over $30 million or has public accountability[3] |

|

2 |

Annual expenses between $2 million and $30 million |

|

3 |

Annual expenses less than or equal to $2 million |

|

4 |

Annual operating payments less than $125,000 |

It is important to note that the XRB is unable to change the $125,000 threshold for Tier 4, as this is determined by the Government in legislation.

Further information can be found here.

[3] In general, an entity is considered to have public accountability if it has issued debt or equity instruments in a public market or holds assets in a fiduciary capacity for a broad group of outsiders as one of its primary businesses – please refer to XRB A1 Application of the Accounting Standards Framework for the full definition.

What is outside the scope of the targeted review of the New Zealand Accounting Standards Framework?

The scope of this targeted review was limited to the ASF itself, being the XRB’s strategy for developing and issuing accounting standards.

Below are the areas that were outside the scope of the targeted review.

|

Out of scope |

Comment |

|---|---|

|

The determination of who should have a statutory requirement to report in accordance with accounting standards issued by the XRB. |

This is determined by the Government through legislation. It is outside of the XRB’s remit. |

|

The appropriateness of specific accounting requirements in accounting standards. |

This targeted review is limited to the ASF, being the strategic framework used to develop accounting standards in New Zealand. It is not a review of the underlying individual accounting standards, or of auditing and assurance requirements. The XRB has other means for receiving feedback on individual accounting standards and assurance requirements. |

|

Audit and assurance requirements |

Outcome

The XRB Board has completed its analysis of submissions received on the Discussion Paper. The responses indicate that in general, application of the framework has not resulted in significant unintended consequences, and that it is operating as intended. Therefore, based on the responses received, the XRB concluded no changes are required at this time.

We have published a Feedback Statement, which outlines the main matters raised by respondents.