Deals with the auditor’s responsibilities in the audit of financial statements relating to going concern and the implications for the auditor’s report.

Applicable for audits of financial statements for periods as indicated. Also applies to subsequent annual reporting periods until that standard is superseded by a new/amended/revised standard. Versions prior to the Previous version below will have been archived.

Previous version

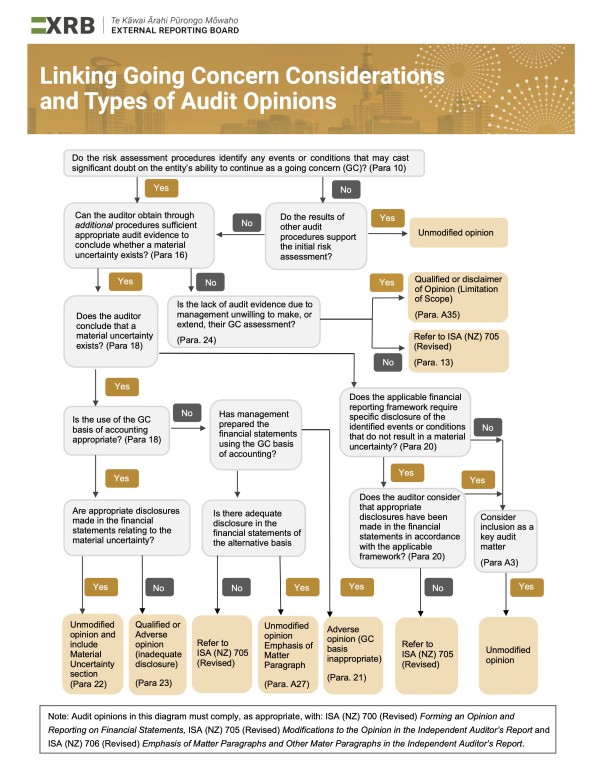

Linking Going Concern Considerations and Types of Audit Opinions |

|

|

Download the PDF below.

|