International updates

6 March 2025

International accounting board members visit New Zealand

Recently, the XRB had the pleasure of hosting two members of international accounting boards, who came to hear what we in Aotearoa thinks about some key international challenges, while experiencing some of the sights and sounds of our country.

International Public Sector Accounting Standards Board (IPSASB) Chair

In February 2025, Ian Carruthers, the Chair of the International Public Sector Accounting Standards Board (IPSASB), visited Wellington, where he had a busy week of presentations, activities, and thought-provoking discussions.

This included presenting to the XRB Board, the New Zealand Accounting Standards Board, and the Sustainability Reporting Board about the international public sector environment and the growing demands for good financial and sustainability reporting. Ian highlighted the significant contribution New Zealand plays in shaping global reporting standards and how New Zealand is leading the way in public accountability and transparent reporting.

Ian Carruthers with fellow panel members, David Eng and prof Sally Davenport.

Ian also got in front of the camera to film some educational videos on the latest IPSAS accounting standards – IPSAS 47 Revenue and IPSAS 48 Transfer Expenses. These videos will be part of the XRB's upcoming Exposure Draft consultations on whether to adopt these standards into the NZ PBE standards. Make sure to subscribe to our accounting alerts to stay in the loop.

The highlight of Ian's visit was an engaging panel discussion on public sector performance reporting in New Zealand. Joined by representatives from the Office of the Auditor-General, New Zealand Treasury, and Victoria University of Wellington, Ian shared his thoughts on the opportunities and challenges in performance reporting. He encouraged public sector entities to keep striving for meaningful and appropriate reporting, even when it's not easy.

Here is the link to the audio recording of the Public Sector Performance Reporting Panel, A Waste of Time or No Time to Waste, hosted by the XRB and Victoria University of Wellington.

International Accounting Standards Board (IASB) Vice-Chair

In November 2024, Linda Mezon-Hutter, the Vice-Chair of the International Accounting Standards Board (IASB), visited Auckland, where she addressed accounting professionals about the IASB's current and upcoming work programme and how the IASB is considering challenges in the rapidly evolving global financial reporting landscape.

Linda, along with IASB technical principal Anne McGeachin and other New Zealand representatives, also discussed the new standard, NZ IFRS 18 Presentation and Disclosure in Financial Statements. NZ IFRS 18 will bring a significant refresh to the financial statements for for-profit entities, and they explored what this means for New Zealanders. This standard has been gazetted and will be effective for reporting periods beginning on or after 1 January 2027.

Watch the IFRS 18 insights panel, which included preparer and auditor views on IFRS 18.

All in all- what a privilege for the XRB having hosted two very distinguished guests in such a short space of time!

Previous Updates

We’re thrilled to announce that the XRB, together with the Australian Accounting Standards Board (AASB), has been jointly appointed to the International Accounting Standards Board’s (IASB) Accounting Standards Advisory Forum (ASAF) for 2025-2027. ASAF is a technical advisory body with the objective of contributing to and assisting the IASB in the global accounting standards-setting process. Being one of only 14 members, we’re excited to share Aotearoa’s perspectives and insights to help shape the future of international accounting standards. This is also a wonderful opportunity to further enhance our Trans-Tasman relationships with the AASB.

21 August 2024

The UK Financial Reporting Council has published a discussion paper on the opportunities for the future of digital reporting in the UK. The paper highlights the growing global appetite for more sophisticated, reliable, accurate and user-friendly digital reporting. The FRC will use the paper to inform their thinking on the taxonomy-related technical and practical implications of policy decisions as well as addressing recent changes in the UK regulatory landscape.

The FRC has been developing and maintaining UK taxonomies for over a decade, providing a framework for high-quality, consistent digital reporting. The UK Taxonomy Suite plays a crucial role in minimising burdens on businesses while supporting economic growth by enabling investors to access and compare information efficiently and allowing regulators to confirm compliance with legal and regulatory requirements.

The taxonomy changes proposed by the FRC could facilitate, among other things:

- replacing block tagging of notes to financial statements with more detailed tagging

- expanding digital tagging to other parts of the annual report, including climate-related and sustainability reporting, and diversity and inclusion information

- the introduction of mandatory assurance over the digital tagging of financial statements.

Digital reporting in New Zealand

The XRB published its position paper on digital reporting in May 2024. The paper highlights that a Government consultation on the possible introduction of mandatory digital financial reporting would be welcomed.

23 July 2024

IFRS 19 Subsidiaries without Public Accountability: Disclosures is a voluntary IFRS Accounting Standard which permits eligible subsidiaries to reduce their disclosures while maintaining compliance with IFRS Accounting Standards.

In light of the existing RDR for Tier 2 for-profit entities in New Zealand, we have considered possible approaches that could be taken to IFRS 19. Our decision has landed on not adopting IFRS 19, but we will consider disclosure requirements in IFRS 19 as part of our decision-making on future RDR concessions. For further information read our IFRS 19 Update.

3 July 2024

The International Accounting Standards Board (IASB) is commencing its comprehensive review of accounting requirements for intangibles.

Intangible assets include things like, copyright, franchise licences, goodwill, trademarks, and trade names, as well as any form of digital asset such as software or cryptocurrency. Since IAS 38 Intangible Assets was developed back in the late 1990’s, it’s fair to say technology and business models (think Uber) have changed dramatically since that time.

The review aims to explore if requirements in the standard are still relevant and reflect current business models or whether the IASB should implement improvements. During the IASB’s Third Agenda Consultation, stakeholders identified this as a high priority project. The initial research and planning phase aims to define the scope of issues to be explored in the project and explore the best approach to plan and organise the work.

For a New Zealand lens on the topic, have a read of the research report by Tom Scott, Laura Mehnaz, and Zeting Zang, or read the recent IASB paper which makes reference to the New Zealand research (see pages 19-20).

15 April 2024

IFRS 18 Presentation and Disclosure in Financial Statements introduces new requirements to improve how information is communicated in the financial statements – in particular, information in the statement of profit or loss.

The XRB is expected to approve NZ IFRS 18 Presentation and Disclosure in Financial Statements in May this year. In the meantime, to get an idea of the changes that NZ IFRS 18 will introduce, read IFRS 18 on one page. Further detail can be found on the IASB’s website.

NZ IFRS 18 will replace NZ IAS 1 Presentation of Financial Statements once it becomes mandatory on 1 January 2027, and is expected to apply to all for-profit reporting entities in New Zealand.

The IFRS Foundation has published a summary of evidence gathered by national standards-setters, including New Zealand, on the effects of guidance on materiality judgements in IFRS Accounting Standards and other materials. Judgements about materiality are essential to the application of IFRS Accounting Standards.

The research showed there is a good understanding of the concept of materiality. Use of the guidance published in 2017 and 2018 varies across jurisdictions; where in use, the guidance has been found helpful. The research also suggested it would be beneficial to continue raising awareness among stakeholders about the guidance.

Read more here.

The International Accounting Standards Board (IASB) expects to publish a new IFRS Accounting Standard on presentation and disclosure (IFRS 18) in April. IFRS 18 replaces IAS 1 Presentation of Financial Statements and introduces some new requirements to improve comparability and transparency of performance reporting. IFRS 18 is relevant to all for-profit entities.

To help stakeholders get ready for this new standard, the IASB has developed a short webcast that provides an overview of the key new requirements in IFRS 18.

Watch the webcast here.

21 January 2024

Australia consults on climate reporting reforms

This month the Australian Government released draft legislation that will establish Australia’s climate-related disclosures framework.

The draft legislation proposes amending the Australian Securities and Investment Commission Act 2001 and the Corporations Act 2001 (Cth) to introduce climate-related reporting requirements for a variety of reporting entities:

For more information visit the Australian Treasury website. Submissions close on 9 February 2024 and can be made to ClimateReportingConsultation@treasury.gov.au

In anticipation of this draft legislation, in October 2023 the Australian Accounting Standards Board issued an Exposure Draft of the Australian Sustainability Reporting Standards for feedback. This consultation closes 1 March 2024.

The External Reporting Board are currently working on a comparison document between Aotearoa New Zealand Climate Standards and the forthcoming Australian Sustainability Reporting Standards. This comparison will outline key differences and areas of commonalities to assist preparers who report in both jurisdictions. It will be published within three months of the publication of the final Australian Sustainability Reporting Standards.

To also help inform New Zealand entities about the Australian requirements, the External Reporting Board will be hosting a number of events in April 2024 where the Australian Accounting Standards Board will discuss the findings of its consultation and the implications for New Zealand preparers. Watch out for more information on our events page shortly.

22 November 2023

IFRS Interpretations Explainer Video

The IFRS Interpretations Committee has released a valuable resource that provides insight into their operations. This short video explains their process when they receive an application question and how they collaborate with the IASB.

It highlights the importance of agenda decisions in supporting the consistent application of the Accounting Standards. The video also emphasizes why companies and others need to consider these decisions when applying the Accounting Standards.

Watch the video here.

30 October 2023

European Sustainability Reporting Mandatory from 2024

The European Parliament has just approved the European Sustainability Reporting Standards (ESRS), making sustainability reporting mandatory for 50,000 companies from January 2024. The ESRS are a central component of the Corporate Sustainability Reporting Directive (CSRD).

Developed by the European Financial Reporting Advisory Group (EFRAG) and integrated into the European legal framework, these 12 sector-agnostic standards are a key part of the Corporate Sustainability Reporting Directive (CSRD). For New Zealand entities operating in the EU, it's important to note that non-EU companies with an annual net turnover of €150M in the EU and at least one subsidiary or branch in the EU will need to comply with sustainability reporting requirements starting 2028. However, the European Commission has proposed a two-year delay on certain aspects, including sector-specific disclosures and reporting from companies outside of the EU.

Access the ESRS on the European Commission website.

10 October 2023

Investor perspectives: IASB Nick Anderson on

cash flow economics

In May 2023 the International Accounting Standards Board (IASB) issued disclosure requirements that enhance the transparency of supplier finance arrangements. These requirements complement requirements in IFRS Accounting Standards for companies to provide disclosures that enable users of financial statements to evaluate changes in debt. The IASB encourages companies to consider early application of the new requirements and to review the effectiveness of their own existing disclosure about changes in debt.

Investors need information about both cash flows and non-cash changes in debt to compare and evaluate companies. IASB member Nick Anderson explains the information companies reporting under IFRS Accounting Standards are required to disclose about non cash changes in debt and how this supports investors in their analysis.

Read the full article here

27 September 2023

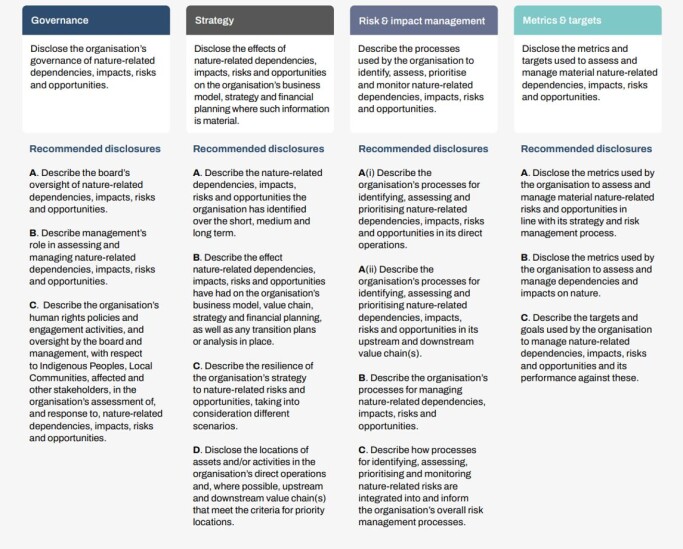

Publication of the final recommendations of the TNFD

This week the final recommendations of the Taskforce on Nature-related Financial Disclosures (TNFD) were published. The TNFD recommendations are intended to “provide companies and financial institutions of all sizes with a risk management and disclosure framework to identify, assess, manage and, where appropriate, disclose nature-related issues”.

The TNFD identifies 14 recommended disclosures which use the same structure as that of the Task Force on Climate-related Financial Disclosures (which themselves form the basis of most climate-related disclosure standards globally). A key difference from the TCFD is the inclusion of ‘impact management’ inside the risk management pillar, and the incorporation within this pillar of ideas such as dependencies on nature. Governance also includes specific reference to human rights.

The TNFD recommendations are voluntary. Concepts of nature and te taiao are being incorporated by the External Reporting Board into our work on developing a non-financial reporting framework for Aotearoa New Zealand. We are however interested in hearing of the experiences of any entities that engage with the TNFD.

Access the final recommendations on the TNFD website.

19 September 2023

The International Public Sector Accounting Standards Board (IPSASB) has announced the appointment of Angela Ryan. Angela’s appointment means that New Zealand continues to be represented on this Board.

Angela, who is Principal Accounting Advisor at the Treasury has over 15 years of experience in applying accrual accounting at the sovereign government level, including the full consolidation of the New Zealand Government financial statements. This will be Angela’s second term on the IPSASB.

Angela has been actively involved in setting accounting standards in New Zealand for many years, both as a member and Deputy Chair of the External Reporting Board’s Accounting Standards Board.

The new IPSASB appointees are selected following a rigorous nominations and interview process involving the IFAC Nominating Committee and IPSASB leadership, overseen by the Public Interest Committee and approved by the IFAC Board. The 2024 Board will continue to be a diverse, woman-majority group, with exceptional public sector accounting experience from around the world.

The IPSASB also announced its new and reappointed Board members and Deputy Chair for 2024, as well as the extension of its Chair through to 2025.

6 September 2023

The IFRS Foundation has recently published a useful overview of its approach to maintaining IFRS Accounting Standards and supporting their consistent application around the world. The overview includes a discussion of the IFRS Interpretations Committee’s activities (such as the publication of agenda decisions) and how these activities contribute to consistent application of IFRS Accounting Standards.

27 June 2023

The IFRS Foundation has published updated educational material to help companies determine how to consider climate-related matters when preparing their financial statements applying IFRS Accounting Standards.

Despite IFRS Accounting Standards not explicitly mentioning climate, companies are required to consider climate-related matters in their financial statements if the effects of those matters are material.

The educational material sets out examples of situations in which companies might need to consider the effects of climate-related matters in their financial statements.

15 March 2023

Source: IFRS website

The International Accounting Standards Board (IASB) has concluded its project on improving its approach to developing and drafting disclosure requirements. The improved approach is designed to help the IASB develop Accounting Standards that would enable companies to make better judgements about which information is material and should be disclosed, thereby providing more useful information to investors.

The improved approach is summarised in guidance that the IASB has published, alongside a Project Summary and Feedback Statement, as part of the IASB’s Targeted Standards-level Review of Disclosures project.

The improved approach involves:

- engaging early with investors to understand their information needs;

- developing disclosure requirements alongside recognition and measurement requirements;

- considering the digital reporting implications of new disclosure requirements;

- using general and specific objectives that describe and explain investors’ information needs; and

- supporting specific objectives by requiring companies to disclose items of information that would satisfy the objectives in most cases.

The IASB intends to use this approach when developing disclosure requirements.

Read more here.

23 February 2023

Source: GRI website

A proposed reporting standard that seeks to unlock accountability for the impacts organizations have on the natural world, informing the global response to a deepening biodiversity crisis, has been made available.

A public comment period for the exposure draft of the revised GRI Biodiversity Standard is underway, with feedback sought so that the final standard delivers the global best practice for transparency on biodiversity impacts.

With the UN Convention on Biodiversity (COP15) starting in Montreal on 7 December – where countries will negotiate a new biodiversity action plan – the timing could not be more critical. Meanwhile, the Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services (IPBES) has warned that biodiversity is declining in every global region.

What this context underlines is that companies face huge demands, from multiple stakeholders, to do more to assess, disclose and reduce their biodiversity impacts. The exposure draft responds to these pressures, building on the latest authoritative insights and extensively revamping the 2016 Standard (GRI 304). It proposes changes that:

-

- Reflect reporting throughout the supply chain, given many biodiversity impacts are found beyond the scope of a company’s own operations;

- Help organizations prioritize attention on their most significant impacts, recognizing the challenge of scale in addressing biodiversity impacts;

- Add new disclosures to connect with the drivers of biodiversity loss, including climate change, pollution, and overexploitation of resources;

- Introduce requirements for biodiversity-related human rights impacts, such as those on indigenous peoples, local communities and workers;

- Emphasise location-specific data, to ensure businesses are transparent about the sites where their biodiversity impacts take place.

Judy Kuszewski, Chair of the Global Sustainability Standards Board (GSSB) – which is responsible for setting the GRI Standards – said:

“It is abundantly clear that biodiversity is under siege, with human activity the leading cause. The affects of biodiversity loss are directly undermining the sustainable development agenda and, if it continues unabated, will have disastrous consequences – on the environment, the economy and people.

Against this backdrop, and on the eve of the UN Biodiversity COP, I’m pleased that our proposal for a major update to the GRI Biodiversity Topic Standard is available for public comment. The revision process has seen an unprecedented level of collaboration with leading experts, so that the final Standard can provide the internationally accepted best practice for transparency on biodiversity impacts.

I encourage all stakeholders and interested parties to participate in this consultation, because we need a standard that will be the global focal point for accountability on biodiversity impacts. Improved reporting – across sectors, regions and supply chains – is crucial for addressing information gaps and informing global solutions."

The revision process saw extensive engagement with other biodiversity frameworks and initiatives, to align the GRI Standard with new developments in the field. IPBES, CDP, the Align project, Partnership for Biodiversity Accounting Financials, and the Accountability Framework were all represented on the technical committee that led the review, while the draft was shaped by input from the Science Based Target Network (SBTN), Taskforce on Nature-related Financial Disclosures (TNFD), and WBA Nature Benchmark.

The exposure draft is open for public comment until 28 February 2023, after which the submitted feedback will be considered ahead of an expected publication date for the final Standard in the second half of next year.

On 15 December, webinars take place where stakeholders can learn more about what’s included in the draft Standard.

As confirmed in December 2021, the revised GRI biodiversity Standard will be used to inform the CDP platform, and input to the TNFD’s financial disclosure framework for nature-related risks. Cooperation and alignment with EFRAG has also taken place on a new EU biodiversity standard (under the Corporate Sustainability Reporting Directive).

A multi-stakeholder Biodiversity Technical Committee, appointed by the GSSB, is leading the revision process for GRI 304, with representatives from:

-

- Mediating institutions: CDP, Deloitte, Global Balance, Lancaster University, Rainforest Alliance, UEBT, UNEP-WCMC

- Business: ConocoPhillips, DSM, L'Occitane, Rio Tinto

- Civil society: BirdLife International, IUCN, Marine Watch International, WWF

- Investors: PBAF, World Bank

- Labor: Department of Conservation – Wellington

GRI thanks KPMG, Ambipar and One Earth for their funding support during the development phase for the update to GRI 304.

COP15 aims to establish a new post-2020 global biodiversity framework. The previous framework resulted in only six of 20 targets being partially met by the 2020 deadline, reinforcing the scale of the challenge.

The recently published KPMG Survey of Sustainability Reporting (October 2022) revealed that, while disclosure using the GRI Standards is widespread, only 40% of 5,800 leading companies around the world currently report on biodiversity.

13 February 2023

An ‘In Brief’ article has been published by the International Accounting Standards Board (IASB) to explain two major decisions that have been made in the Business Combinations—Disclosures, Goodwill and Impairment project.

Rika Suzuki, IASB member, discusses the reasons for the IASB’s decisions about how companies could disclose better information about mergers and acquisitions (business combinations), and whether to retain the impairment-only model to account for goodwill or to explore reintroducing amortisation of goodwill.

Business Combinations—Disclosures, Goodwill and Impairment is now a standard-setting project, which involves the preparation of an exposure draft that contains proposals of amendments.

Read the full article here

29 November 2022

Online or in Montreal

Join global businesses, investors and policymakers to discuss progress towards a global baseline of sustainability disclosures to inform investment decisions, including discussions on:

- themes of feedback received on the exposure draft standards and progress towards publishing the final standards

- the prospect for regulatory adoption of the IFRS Sustainability Disclosure Standards

- the need for capacity building for both emerging economies and small and medium-sized companies

- preparedness of investors and corporates to use and disclose with the standards, and

- #integratedreporting best practices and use cases.

Find out more and register here

#globalbaseline #sustainabilitydisclosures #capitalmarkets #IFRSSustainability23 IFRS Foundation

7 September 2022

The accounting standard which addresses intangible assets (IAS 38 Intangible Assets) was issued in the late 1990s and remains substantively the same. Since the 1990s the world has changed significantly, creating many new types of intangibles, not originally contemplated when the standard was written. Stakeholders, both in New Zealand and internationally, have raised concerns about this. These concerns have been noted and there is a current international call for research into various aspects of the accounting for intangible assets, to provide evidence to assist in a comprehensive review of IAS 38.

To understand the New Zealand perspective and, as part of its contribution to the international discussion, the XRB invites proposals for research projects relating to the accounting for intangible assets. A research grant of NZ$5,000 will be available.

Proposals to be submitted by 14 October 2022.

For more information click here

2 August 2022

Our feedback to the ISSB on its first two proposed IFRS Sustainability Disclosure Standards signalled broad support for the drive towards global consistency and the development of a global baseline for sustainability reporting.

The XRB submission has been informed through the extensive consultation and engagement we have undertaken over the past 18 months on Aotearoa New Zealand’s climate-related disclosure framework, and key highlights of our feedback include:

- Taking a more principles-based and less prescriptive approach to the development of both proposed standards

- Raising the ambition and working towards ‘one pillar’ for sustainability reporting, rather than setting out to create two pillars (i.e., a focus on capital markets and investors by the ISSB, and a focus on multi-stakeholder reporting by the GRI) that are interoperable

- Not permitting alternatives to scenario analysis

- Not mandating industry specific metrics

- Moving the disclosures on offsets from transition plans to greenhouse gas emissions reductions targets

Find out more by reading the full submission here.

26 July 2022

The International Auditing and Assurance Standards Board (IAASB) are currently consulting on narrow scope amendments to ISA 700 (Revised), Forming an Opinion and Reporting on Financial Statements and ISA 260 (Revised), Communication with Those Charged with Governance.

These amendments have been proposed as a result of the International Ethics Standards Board for Accountants’ (IESBA) revisions to the International Code of Ethics, that require a firm to publicly disclose when the Public Interest Entity (PIE) independence requirements have been applied in an audit of financial statements.

In the New Zealand context, adopting these proposals would mean that where the PIE requirements are applied, the auditor’s report will be required to disclose this as well as disclosing that the auditor is independent of the entity.

You can submit your comments to the XRB by 16 September 2022, or directly to the IAASB (now closed), with a copy to the XRB, by 4 October 2022.

13 June 2022

Making materiality judgements is an important but not always straight forward aspect of preparing financial statements.

In partnership with the XRB, the IASB is calling for academic proposals for research that will help inform the IASB's next steps in addressing the ‘disclosure problem’. The objective of the research is to provide information to enable the IASB to assess the effects of recent guidance on making materiality judgments on preparers, investors, auditors, and regulators.

A research grant of NZ$5,000 will be available.

Improving disclosure practice - the IASB's Disclosure Initiative

There are some concerns that preparers may be taking a ‘boilerplate’ approach to the preparation of financial statements and not applying appropriate judgement when selecting the most meaningful, useful, and relevant information to disclose. But making sound materiality judgement can be difficult because different readers or users of financial reports will inevitably have different information needs.

The International Accounting Standards Board (IASB) are looking at ways to improve this through their Disclosure Initiative project which will focus on addressing the following three main concerns highlighted by stakeholders:

- not enough relevant information;

- too much irrelevant information; and

- ineffective communication of the information provided.

Submissions of interest to the XRB closes on July 2022.

14 April 2022

The International Sustainability Standards Board (ISSB) has recently published its first two proposed IFRS Sustainability Disclosure Standards which when final, will form a comprehensive global baseline of sustainability disclosures designed to meet the information needs of investors when assessing enterprise value. The proposals for Climate-related Disclosures will establish disclosure requirements for climate‑related risks and opportunities.

Emmanuel Faber, the Chair of the ISSB introduces the proposals in a short video here.

For those of you short on time, there is a handy snapshot document here.

Overview of the ISSB Proposals

The two proposed standards are IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information and IFRS S2 Climate-related Disclosures.

IFRS S1 applies to all sustainability topics not just climate. This means that from day 1 even in the absence of the other ISSB Standards, entities would have to follow a high-level framework for disclosing information about all sustainability topics that are material to them.

IFRS S2 is the ‘climate’ standard and is to be applied in conjunction with IFRS S1. IFRS S2 proposes requiring an entity to disclose information that would enable an investor to assess the effect of climate-related risks and opportunities on its enterprise value.

The draft standards build on the prototypes previously published by the IFRS Foundation’s Technical Readiness Working Group (TRWG).

The requirements in IFRS S2 are consistent with the four recommendations and 11 recommended disclosures published by the Task Force on Climate-related Financial Disclosures (TCFD). IFRS S2 does include some additional specific disclosures for example, in requiring disclosure of industry-based metrics relevant to an entity’s industry and activities.

The ISSB consultation

The ISSB’s consultation is open for comment until 29 July 2022. The ISSB plans to issue the standards before the end of 2022 when they will be available for immediate voluntary adoption.

The ISSB asks for submission letters, or survey responses. Note that the ISSB has set up separate consultation platforms for each exposure draft.

XRB staff will be responding to the request for comments. If you do submit on the proposals, please send a copy of your submission letter to the XRB at climate@xrb.govt.nz.

To read the ISSB’s proposals in full:

ISSB - Climate-related Disclosures consultation

ISSB - General requirements for Sustainability-related Disclosures consultation

25 March 2022

This week, the United States Securities and Exchange Commission (US SEC) released their proposed framework for mandatory climate-related disclosures for public consultation.

Similar to the XRB’s mandate to deliver a climate-related disclosure framework for Aotearoa New Zealand, this proposal aims to ensure both domestic and foreign entities are disclosing climate-related information, including financial risks and climate related metrics, in their US financial statements.

Overview of the US SEC proposals

The proposal requires registrants to disclose:

- Governance of climate-related risks and relevant risk management processes;

- The number of climate-related risks that have or are likely to have, a material impact on its business and consolidated financial statements over the short, medium, or long-term;

- How any identified climate-related risks have affected or are likely to affect strategy, business model, and outlook;

- The process for identifying assessing and managing climate related risks;

- The impact of climate-related events (severe weather events and natural conditions) and transition activities on the line items included in the consolidated financial statements, as well as on the financial estimates and assumptions used in the financial statements;

- Scope 1 - Direct greenhouse gas (GHG) emissions and Scope 2 indirect GHG emissions from purchased electricity or other forms of energy;

- Scope 3 - Disclose GHG emissions from upstream and downstream activities in its value chain if material or if the registrant has set a GHG emission target or goal that includes scope 3 (noting that smaller registrants are excluded from scope 3 emissions disclosures); and

- Climate-related targets or goals, and any transition plan, if any.

Close alignment to NZ’s proposed disclosures

As with New Zealand, SEC’s proposals are modelled on the recommendations of the Task Force on Climate-Related Financial Disclosures (TCFD). This includes the same four key areas of Governance, Risk Management, Strategy, and Metrics and Targets, as well as drawing on the GHG Protocol. This is similar to the proposals made by the IFRS Foundation’s Technical Readiness Working Group (TRWG). (See here for a comparison between the XRB, TCFD and TRWG disclosures).

Key differences

There are minor differences between the XRB’s proposals and those of the US SEC. Included in the US SEC disclosures are:

- The addition of the qualifier ‘if used’ on many of the disclosures

- A phase-in period for scope 3 emissions disclosures (including for smaller companies) up to fiscal year 2025 for some entities

- An explicit requirement for a direct link between climate disclosures and financial statements: “the impact of climate-related events (severe weather events and other natural conditions) and transition activities on the line items of a registrant’s consolidated financial statements, as well as on the financial estimates and assumptions used in the financial statements”

- A requirement to disclose about offsets and renewable energy certificates: “If carbon offsets or renewable energy certificates (“RECs”) have been used as part of the registrant’s plan to achieve climate-related targets or goals, certain information about the carbon offsets or RECs, including the amount of carbon reduction represented by the offsets or the amount of generated renewable energy represented by the RECs”

The consultation

The US SEC consultation is open for comment until 20 May 2022. If approved the US SEC intends to implement these changes to reporting from 2024.

To read the proposal in full, click here.

28 January 2022

The IAASB have recently announced that they will dedicate capacity and resources to the assurance of sustainability/ESG reporting.

Information gathering and research activities to determine future IAASB action has commenced in January this year, with initial work underway to determine scope and timing. The IAASB have also signalled a strong commitment to collaborate with key stakeholders globally, including the standard-setting and regulatory communities.

Their consultation could lead to:

- Development of new subject-matter specific standard(s) that build on and supplement ISAE 3000 (Revised);

- Targeted enhancements to ISAE 3000 (Revised), as necessary; or

- Revising existing guidance or developing new guidance.

In 2021, we published the IAASB’s comprehensive guidance to support application ISAE 3000 (Revised) to Extended External Reporting (EER) Assurance Engagements along with a navigation tool to help point users to relevant chapters.