The main activity of the IFRS Interpretations Committee (the Committee) is responding to questions about the application of IFRS Standards. The Committee response may include developing explanatory material or recommending that the International Accounting Standards Board (IASB) amend the existing

IFRS Standards.

IFRS Interpretations Committee

It is important to understand the status of decisions made by the Committee because they may impact how you go about preparing your financial statements in compliance with

NZ IFRS.

Although agenda decisions are specifically developed with for-profit entities in mind, public sector or NFP public benefit entities (PBEs) applying Tier 1 or Tier 2 PBE Standards may also consider applicable explanatory material in the Committee's agenda decisions when developing and applying accounting policies in accordance with PBE IPSAS 3.

Process and Status of Agenda Decisions

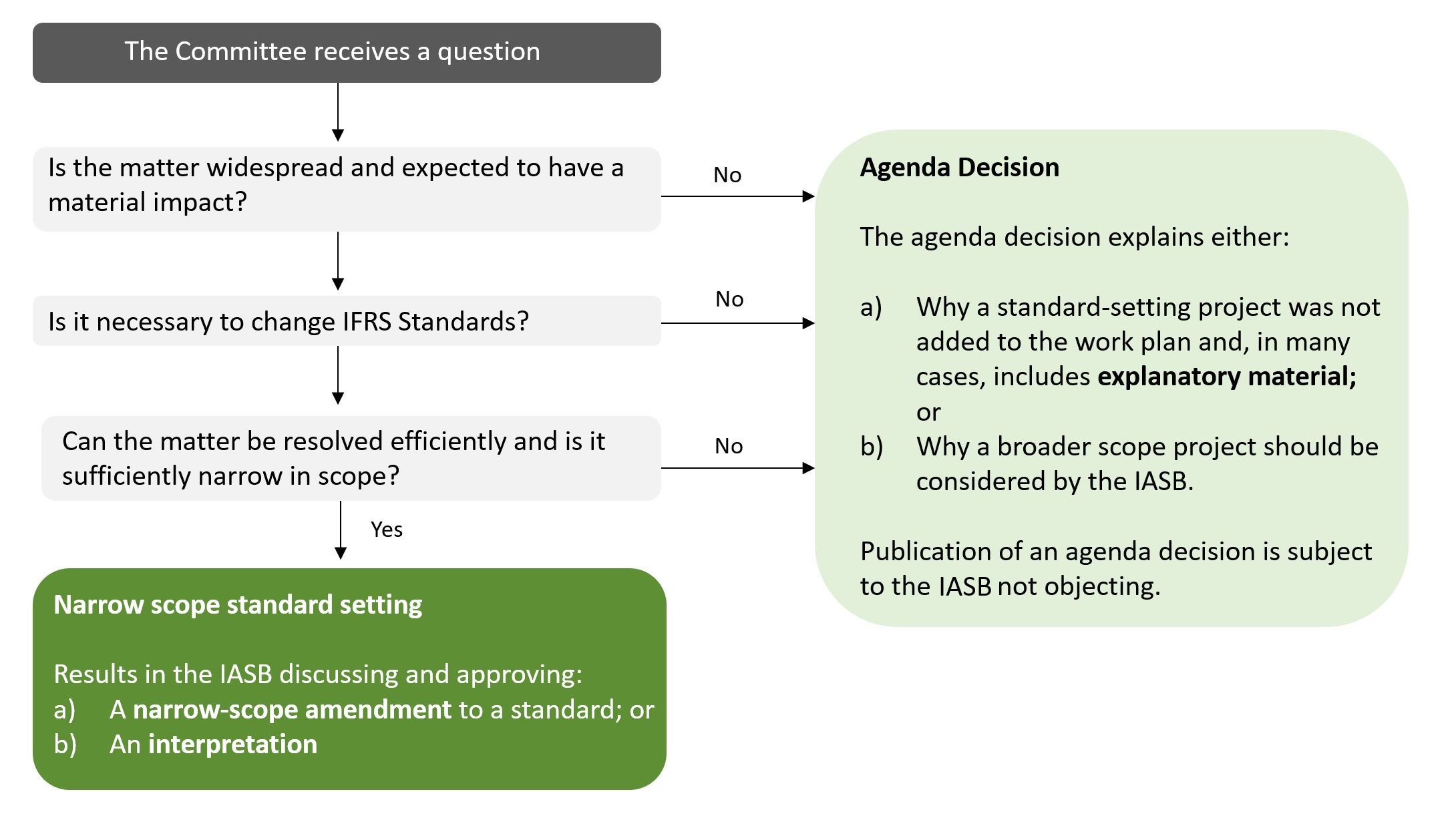

The diagram below provides a summary of the Committee process when responding to questions received.

When preparing NZ IFRS compliant financial statements, consideration should be given to applicable explanatory material in agenda decisions.

If the Committee decides not to add a standard-setting project to the IASB’s work plan, then it issues an ‘agenda decision’ that explains why and often outlines how to apply the principles and requirements of IFRS Accounting Standards to the questions received by the Committee.

Agenda decisions cannot add or change requirements in IFRS Accounting Standards, but rather aim to improve consistency in their application. The explanatory material in an agenda decision derives its authority from IFRS Accounting Standards and often provides additional insights on how to apply them. Therefore, to be able to assert compliance with IFRS Accounting Standards, entities are expected to change their accounting policy to the extent that their accounting differs from that described in the agenda decision.

Agenda decisions do not have an effective date or any transition provisions because they do not change any principles or requirements in existing accounting standards. They are expected to be applied as soon as possible and any required accounting policy changes are expected to be applied retrospectively.

Implementing agenda decisions may sometimes be difficult – especially when an agenda decision is issued near a reporting date and requires a change to an entity’s existing accounting policies. This is because effecting an accounting policy change may require entities to undertake a number of steps, such as collecting additional information to apply the new policy or provide disclosures, or changing processes

or systems.

The IASB has confirmed that an entity is entitled to sufficient time to determine whether to change an accounting policy as a result of an agenda decision and to implement any such change. Determining ’sufficient time’ will require the application of professional judgement, based on facts and circumstances specific to the entity.

Recent IFRS Interpretations Committee Activities

The IFRS Interpretations Committee publishes tentative agenda decisions for comment before finalising those decisions. Click on the links for more information on recent tentative and final agenda decisions.

Accessing All IFRS Interpretations Committee Agenda Decisions

You can search agenda decisions by date and by standard.